Executive Summary

- Indian government bonds are a stable source of carry/income. Its high yields, strong domestic demand and low foreign ownership level make Indian bonds less volatile than US bonds.

- Improved foreign investor accessibility, market liquidity and depth as well as better fiscal management have also contributed to the bonds’ attractiveness.

- In the near term, the outlook for India’s government bonds is supported by prospects of rate cuts by the Reserve Bank of India, given India’s moderating growth momentum and more controlled inflationary pressures.

The inclusion of Indian government bonds in the JP Morgan Global Emerging Market (EM) Bond Index was one of the biggest developments within the global emerging bond markets in 2024. Starting from 28 June 2024, the weightage of Indian governments bonds is set to increase by 1% each month until it accounts for 10% of the index. In 2024, Bloomberg and FTSE also announced that they will be adding Indian government bonds to the Bloomberg EM Local Currency Government Index plus related indices as well as in the FTSE EMs Government Bond Index starting from 31 January 2025 and September 2025 respectively.

Indian government bonds’ inclusion into the global bond indices is expected to attract substantial foreign investment, with estimates ranging from USD 20 to 40 billion1.

Coming of age

The inclusions into these global bond indices represent the coming of age for India’s bond market, which is the second largest in the world behind the US. As of September 2023, the government bond market size stands impressively at USD1.3 trillion, with corporate bonds at USD0.6 trillion. However, foreign portfolio investment in these markets is relatively modest at USD8.5 billion.

The inclusions are the result of years of efforts by the Indian government to improve foreign investor accessibility, market liquidity and depth, which includes:

- The Fully Accessible Route (FAR) framework, which was introduced in March 2020 allows non-residents to invest in specified government securities without investment caps.

- The Reserve Bank of India (RBI) has periodically adjusted the list of securities eligible under the FAR framework, thereby increasing the range of options for investors.

- Investments in market infrastructure, such as better trading platforms and more efficient settlement systems.

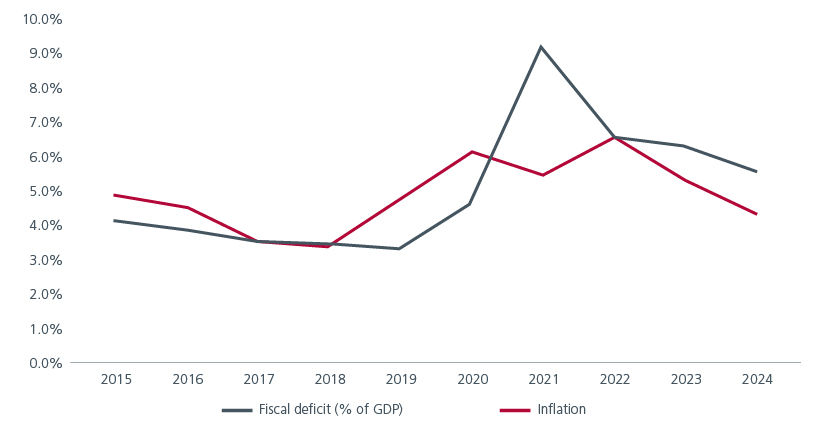

At the same time, better fiscal management, lower currency volatility and an improved inflation outlook in recent years have helped to increase the appeal of Indian government bonds. Over the last 10 years, India’s fiscal deficit has shown a trend of consolidation except for the COVID-19 pandemic period, when the deficit surged to around 9.5% of GDP on the back of increased government spending on relief measures and a decline in revenue. Meanwhile, India’s inflation has averaged between 4% to 6% over the same period. See Fig. 1.

Fig. 1. India’s fiscal deficit as a % of GDP and inflation

Source: Reserve Bank of India. January 2025.

The attractiveness of Indian government bonds

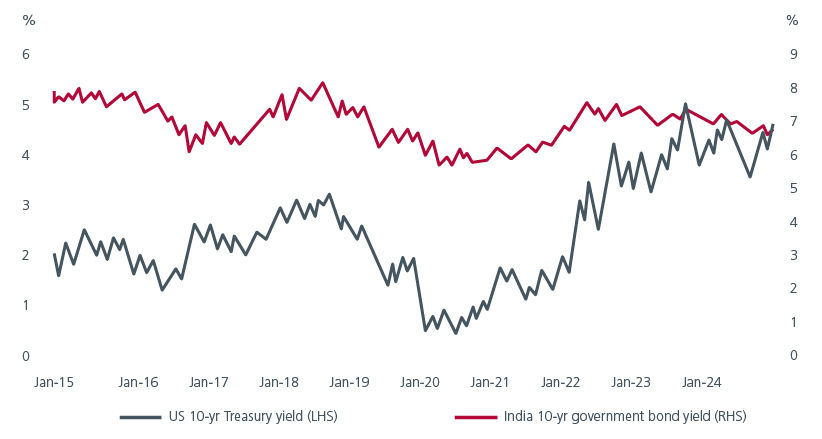

In our view, Indian government bonds provide stable income/carry. Indian government bonds offer relatively higher yields compared to bonds from many other emerging markets. In addition, given their still-low foreign ownership level (5%2) and strong demand from domestic insurance and pension funds, Indian government bond yields have demonstrated less volatility compared to US yields. See Fig. 2. The reduction in the face value of bonds ₹10,000 and the emergence of Online Bond Platform Providers have also made it easier for domestic retail investors to participate in the bond market, further boosting the demand for Indian government bonds.

Fig. 2. US vs India 10-year government bond yields (local currency terms)

Source: Bloomberg. January 2025.

Moreover, for equity investors with existing Indian equity exposure, adding Indian government bonds can help lower portfolio volatility while still benefiting from India’s long-term economic reforms.

With the inclusion enhancing India’s visibility and credibility in the international financial community, the government will need to maintain fiscal discipline or risk suffering foreign investor outflows. In addition, having a healthy government bond market will create positive spillover benefits for Indian corporates. Lower bond yields may lower borrowing costs and improve profitability. A robust government bond market may also free up the banking sector’s capacity to increase its lending to the private sector as well as provide funding for infrastructure projects, which can boost long-term economic growth.

Positive near-term outlook amid potential risks

In addition to the long-term drivers mentioned above, the near-term outlook for India’s government bonds appears promising. India’s growth momentum is moderating, and inflation is expected to be more contained in 2025 compared to prior years. Unlike other Asian central banks, the Reserve Bank of India (RBI) did not start cutting rates in 2024. This potentially gives the RBI more room to cut rates in 2025 when the opportunity arises, which should be supportive of bond prices.

That said, we are mindful of the potential risks posed by a strong USD and fluctuating US bond yields. Higher than expected spending by the Modi government to stimulate short-term economic growth could also challenge fiscal discipline and increase the supply of Indian government bonds. Despite these concerns, we believe that Indian government bond yields can trend lower over the medium term due to strong demand from both foreign and domestic investors, robust long-term economic fundamentals, and a strengthened banking sector. Active investing would be key to capitalise on the opportunities to extend duration when these market concerns are temporarily elevated.

Interesting reads

Sources:

1 Bloomberg. June 2024.

2 Foreign ownership of FAR-designated bonds – which constitutes 40% of IGB issuance – as at June 2024. JP Morgan Research.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.