Summary

Divergent data and concerns over China’s growth are being tempered by more concerted government action. In the meantime, while the US’ Magnificent 7 has hogged headlines, a handful of stocks in Asia has actually done even better.

What’s top of investors’ minds

1. What will be the impact of Trump's policies on US rates?

Looking at history, it is worthwhile to note that US rates are influenced by a combination of 1) local development (growth/inflation), 2) the influence of external events on local dynamics and 3) funding patterns.

The first and most significant phase of the US rates selloff has happened. While yields may still creep higher as tariffs are announced, any further increases from current levels will likely be more tepid as tariff policies are gradually being priced in prior to their official announcement/confirmation.

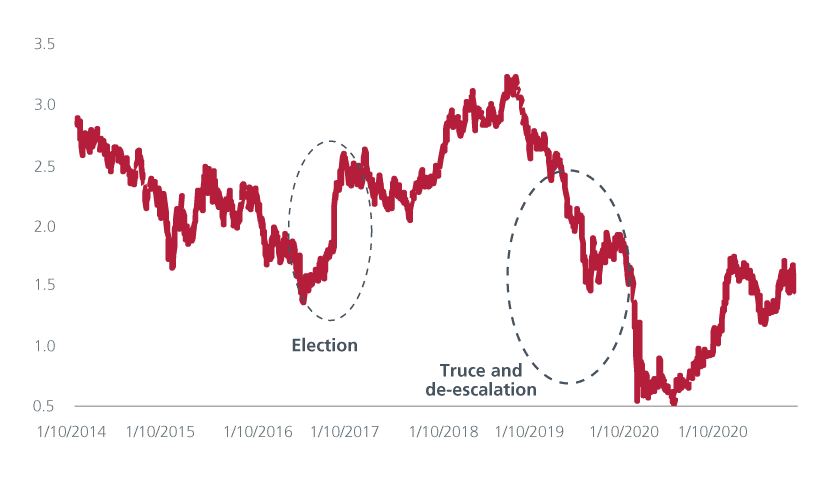

History suggests that a rates selloff due to tariffs tends to temporary as tariffs are seen as a “negotiating tool” to help balance trade. Rates and FX volatility were higher during the period of tariff escalation for most of FY2018 - the magnitude of the move this time is more subdued as the impact is spilt/absorbed across asset classes. Additionally, countries are better prepared to retaliate. This could dampen the tariffs' intended impact or reduce the level of US aggression. Ultimately, a truce/de-escalation phase would be highly positive for markets.

We view this current episode as offering a potential trading opportunity, first for investors to short US rates and subsequently to go ‘long’ when signs of de-escalation emerge (the speed of transition in Trump 2.0 may be faster than Trump 1.0).

Aside from the tariff impact, we note that the US economy was already slowing going into the election. With inflation rates averaging around 2% or higher and US rates at 4% - and the highest real rate in almost 2 decades - investors have a healthy buffer. The recent nomination of Scott Bessent for Treasury Secretary also illustrates that while the US wants to escalate to de-escalate trade policies, they are also concerned about high US interest rates and deficits. Bessent, in a recent interview, indicated that he would like to raise US economic growth to 3%, reduce the fiscal deficit to 3% of GDP and increase US oil production by 3mn barrels/day. These goldilocks targets, if achieved, could put downward pressure on both rates and inflation.

US 10-year treasury yield (2016-2020)

2. What next for the Chinese economy?

Divergent data and concerns over the growth path are being tempered by, arguably, more concerted government action.

It has been a tricky time attempting to gauge a likely path for the Chinese economy in 2025. Data over recent weeks has painted a positive picture for manufacturing PMI through the Caixin survey, yet official data was more subdued showing the dividing line potentially between private companies and more state-focused enterprises. As we head into December, concerns over housing and tariffs have weighed on confidence with various forecasts for Chinese GDP being revised below 5% for both 2024 and 2025. Perhaps critically, trade data has continued to show a wide gap - exports grew 6.7% year on year but imports fell 3.9% over the same period.

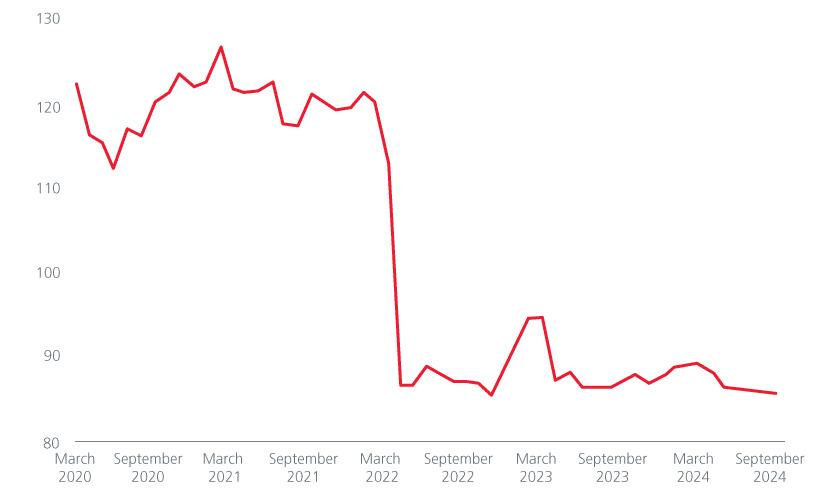

Against this slightly tepid backdrop, the question most commentators have asked is whether the central government will step forward with much more meaningful monetary stimulus. This fiscal impact could help to encourage the domestic consumer and stabilise growth; a chart in our 2025 market outlook paints the current picture for consumer confidence in China quite clearly.

Addressing the housing crisis may have been one focus connected to initial stimulus, but this does not appear to have moved to the broader economy where consumer confidence is muted, and savings rates remain high. Unlocking the potential within the consumer appears key for growth and confidence in 2025.

China consumer confidence

3. Broadening the rally?

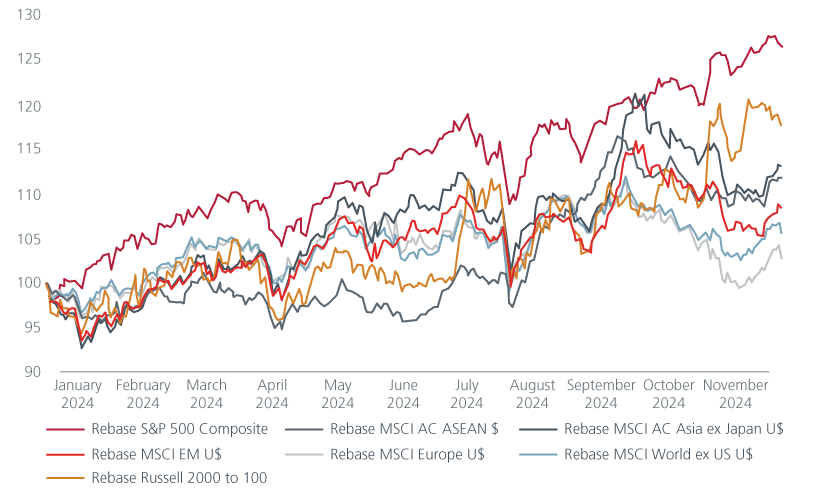

Investors could arguably have done pretty well by buying a very small selection of US stocks to drive their performance, or so the headlines read.

Recent data from Morgan Stanley showed that approximately 20-25% of companies within individual markets such as China, India, Korea and Taiwan, did better than the magnificent 7 in 2024. If you then consider market capitalisation, this increases the impact, for example in markets like Taiwan and Singapore.

Significant valuation discounts still exist between the large cap US stocks and markets beyond the US – selective stock picking would have offered good gains in 2024. What is the chance that more of this persists in 2025? The rally may broaden to the small and mid -cap area of the Japanese market. Selected ASEAN markets still have considerable potential, particularly those that benefit from favourable long-term themes and arguably lesser impact from tariffs.

Equity market performance (2024)

Data source: LSEG Datastream, Eastspring Investments (Singapore) Limited. The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future or likely performance of the Fund. The latest data provided is as of 11 December 2024.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.