Jie Lu

Portfolio Manager,

Quantitative Equity Strategy,

Eastspring Investments, Singapore

Aug 2023 | 5 min

Michael (Xiaochen) Sun

Director, Quant Capability,

Client Portfolio Manager,

Quantitative Strategies,

Eastspring Investments

Summary

“The whole is greater than the sum of its parts” – Aristotle

Aristotle's famous quote indicates the essence of successful investment strategies. It acknowledges the fact that the total effect of integrated elements often generates superior outcomes compared to the added contributions of each isolated component.

This holistic view recognises the value of interactions between parts and hence fundamentally resonates with the principles of multi-factor investing. In addition, this perspective also underpins the concept of diversification more generally, which in the current environment deserves more attention in investment portfolios.

Unveiling concentration risk

Financial markets have witnessed a tumultuous first half of 2023, characterised by a range of notable events. From a surge in tech stocks driven by artificial intelligence (AI), to market volatility in commodities and cryptocurrencies, and even a severe banking crash reminiscent of the Lehman Brothers collapse. However, what sets this period apart is the persistent rise in interest rates, which has been a departure from the market conditions experienced in 2022.

Despite the challenging environment, global stocks, as measured by the MSCI ACWI, have managed to rally by approximately 14%. 1 Yet, this rally has been accompanied by a significant concentration of value appreciation within specific sectors. The AI boom, buoyed in part by advancements in technology like ChatGPT, has pushed the "Mega Tech" giants such as Apple, Microsoft, Alphabet (Google's parent company), Amazon, and Netflix to impressive gains of 35% to 50%, as shown in Fig 1.

Notably, Meta and Tesla have more than doubled in value, while the soaring demand for semiconductor chips driven by AI applications has catapulted Nvidia's stock price by a staggering 185%, briefly propelling it into the exclusive club of U.S. companies with a market value surpassing $1 trillion.

Fig 1: The magnificent seven dominated the upside

Source: Refinitiv Eikon, S&P Global, and Eastspring Investments, June 2023

This prevailing trend of mega-cap stocks dominating the market significantly amplifies the concentration risk within the equity market. Consequently, there is a heightened level of risk associated with the market due to its concentrated nature.

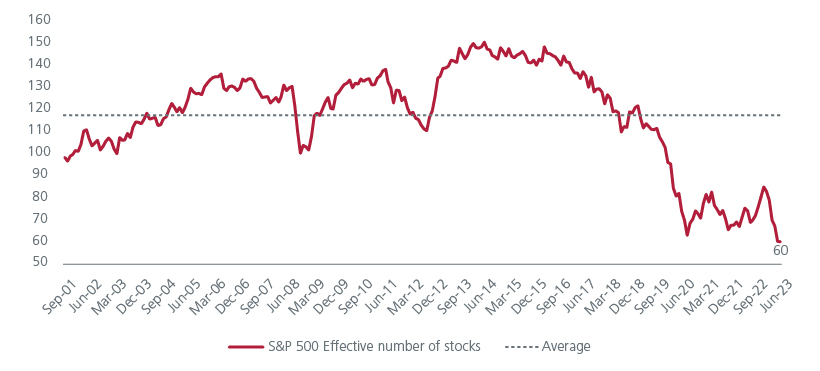

To quantify the extent of market concentration, we can utilise the concept of the effective number of stocks. This metric provides a simple measure of index concentration, ranging from 1 (indicating complete concentration in a single stock) to N, representing the total number of constituents in the index. A low effective number of constituents indicates a high level of index concentration.

Notably, as shown in Fig 2, the effective number of companies within the S&P 500 index has witnessed a persistent decline since March 2018, reaching an unprecedented low of only 60 effective stocks by June 2023. This level is significantly below the pre-pandemic low of 96 recorded during the dot-com bubble period, highlighting a reduced level of diversification, and underscoring the critical need to evaluate concentration risks meticulously.

Fig 2: Historical low hit of effective number of stocks

Source: Bloomberg, S&P Dow Jones Indices, and Eastspring Investments

Recognising the concentration risk, market cap index providers have taken action. For example, the Nasdaq-100 Index, the underlying index for Invesco QQQ Trust (QQQ), the world's fifth-largest exchange-traded fund (ETF), underwent a special rebalance on July 24.

This rebalance aimed to address the over-concentration of the index, particularly among the "Magnificent Seven" companies, including Microsoft, Apple, NVIDIA, Amazon, Tesla, Meta Platforms, and Alphabet, which collectively represent nearly 55% of the index as of June 2023.

The special rebalance did not involve the removal or addition of securities but instead focused on reducing the index's concentration in its largest constituents. This move serves as a reminder of the risks associated with over-reliance on a narrow market leadership.

The enduring importance of diversification

Diversification, as advocated by Harry Markowitz's renowned statement that "Diversification is the only free lunch," plays a crucial role in managing risk and optimising portfolio performance. In 1952, Harry Markowitz revolutionised the field of portfolio management with his dissertation on "Portfolio Selection2 ," which laid the foundation for Modern Portfolio Theory. His insights highlighted the goal of maximising returns for a given level of risk, achieved through the incorporation of less correlated securities into a portfolio. Markowitz's ground-breaking formula enabled investors to mathematically balance risk tolerance and reward expectations, ultimately constructing an optimal portfolio.

While the benefits of diversification have long been recognised across individual stocks and asset classes, the concept extends beyond these boundaries. With the development of financial literature and theoretical frameworks, such as Robert C. Merton's Intertemporal Capital Asset Pricing Model (ICAPM)3 , the focus shifted towards diversification among factors. This evolution facilitated the emergence of multi-factor investing, allowing investors to enjoy the benefits of factor exposure while reducing overall deviation from the benchmark.

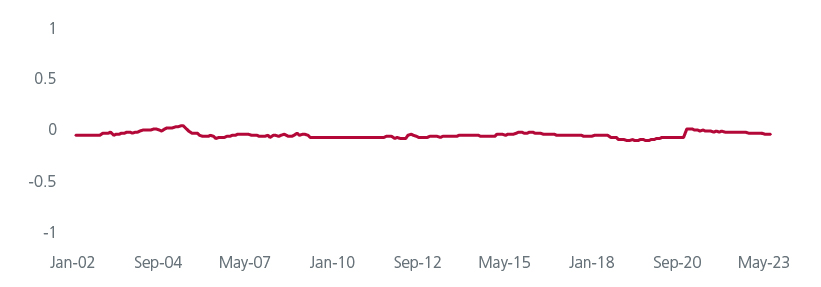

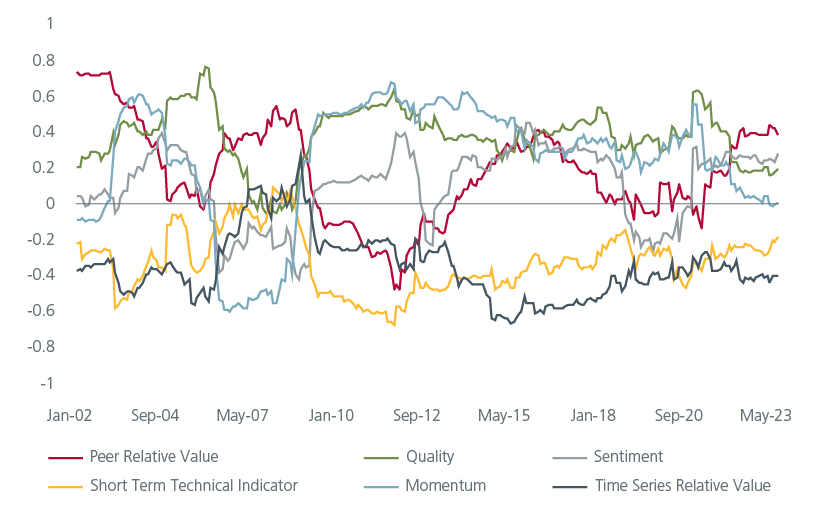

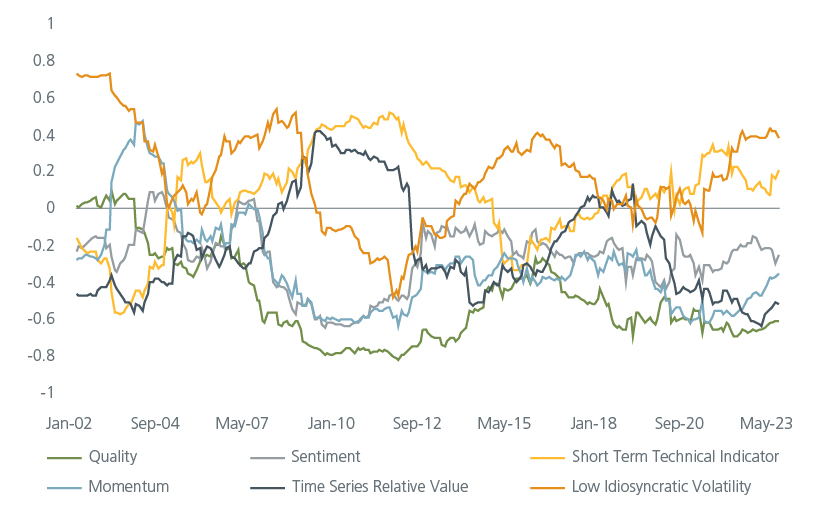

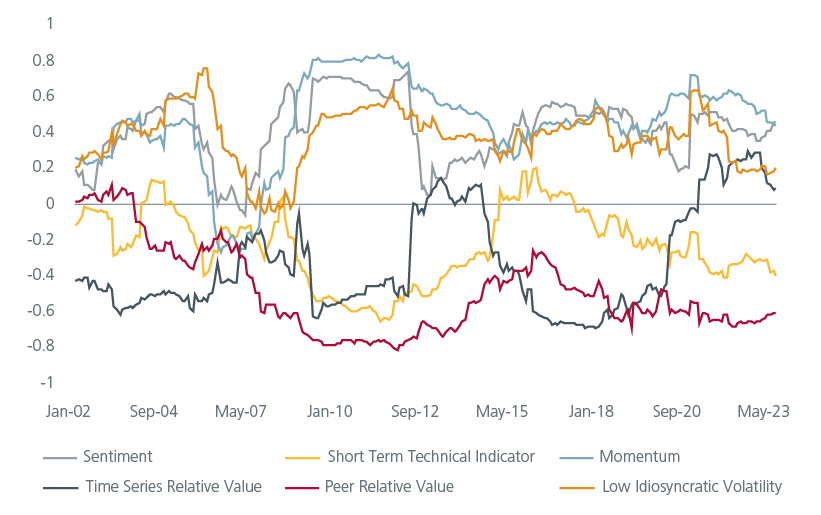

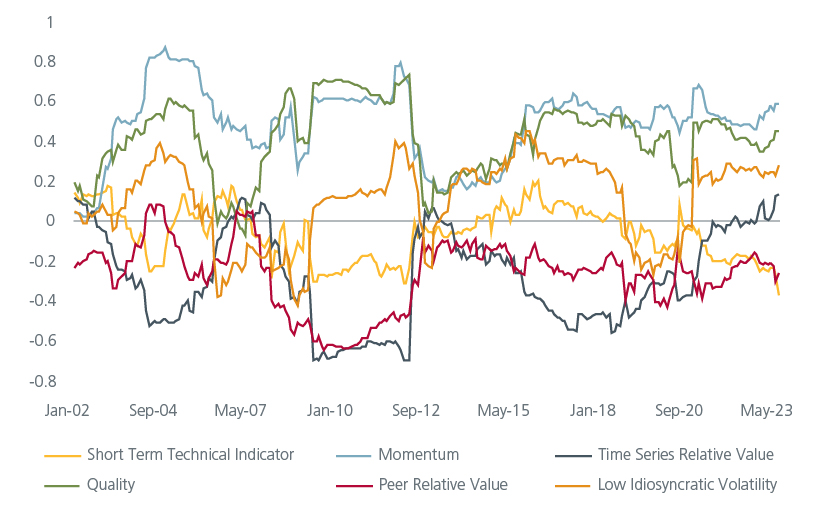

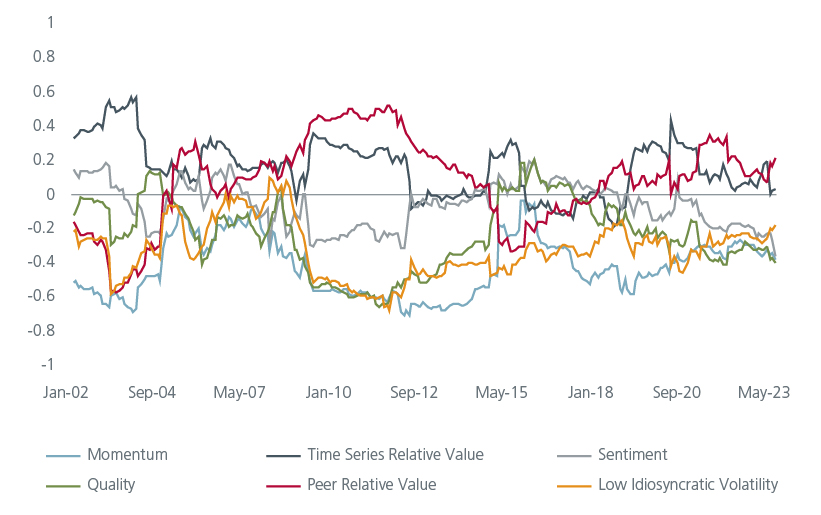

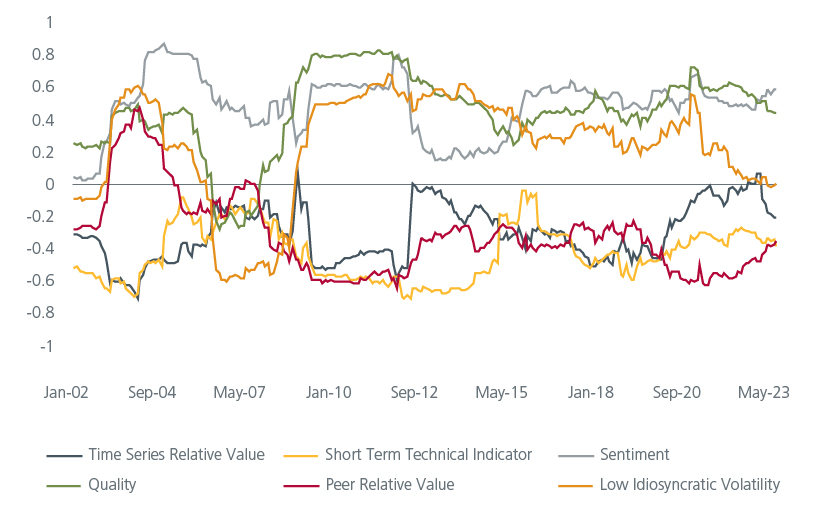

In a multi-factor equity investment strategy, the focus lies in selecting factors with low correlations to each other, ensuring enhanced diversification and potential risk reduction within the portfolio. In Fig. 3 (shown at the end of this article) and Fig. 4, we have presented a group of well-established risk premium factors (with our own enhanced definition). These factors make up a diverse collection of stock return drivers that are not strongly correlated with each other (Fig. 3), as indicated by the average pairwise correlation of their returns over a 3-year rolling period in Fig. 4.

Fig 4: 3-year rolling average pairwise correlation of factor returns

Source: Bloomberg, S&P Dow Jones Indices, Refinitiv, and Eastspring Investments

Building in resiliency to the cyclicality of individual factors

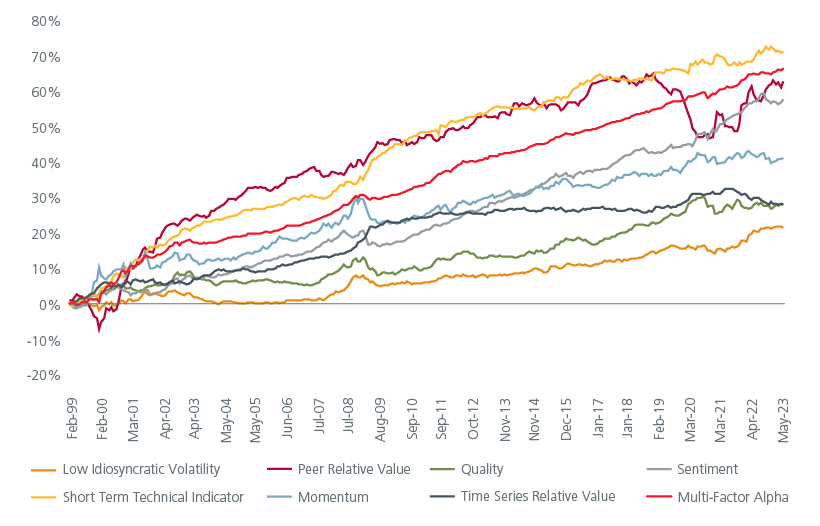

Factors such as Value, Quality, Momentum, and Low Volatility offer distinct return characteristics, enabling investors to capture broader market trends. While we expect our individual alpha factors to generate long-term returns, as illustrated in Fig 5, it is important to note that they may exhibit cyclical performance in the short term. However, the short-term returns of these factors do not move together due to their contrasting exposure to the economic cycles. Fig 6.

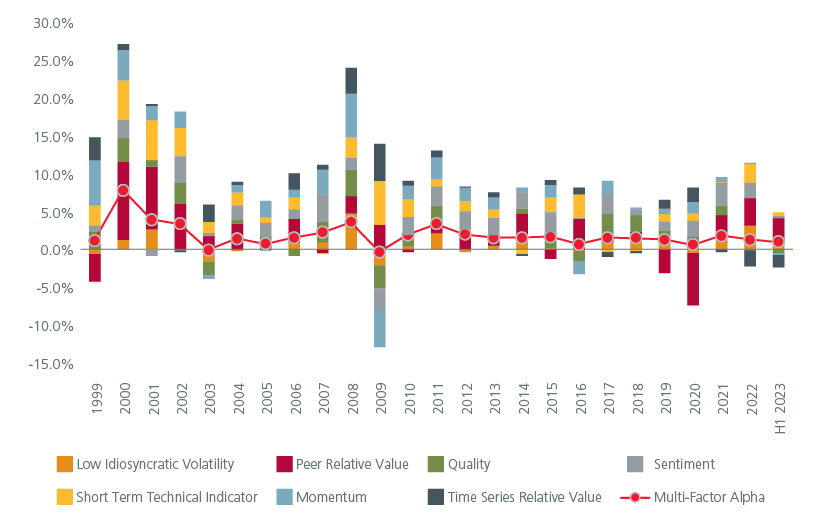

By targeting a broad exposure to cyclical, defensive, and dynamic factors, a well-formed multi-factor strategy benefits from diversification, enabling participation in the long-term outperformance of individual factors while mitigating the cyclicality associated with each factor. With a multi-factor strategy, investors not only gain exposure to various investment themes but also mitigate the concentration risk associated with relying on a single factor. This approach allows for the benefits of factor investing while effectively managing deviations from the benchmark.

Fig 5: Single factors’ long-term performance

Source: Bloomberg, S&P Dow Jones Indices, Refinitiv, and Eastspring Investments

Fig 6: Multi-factors’ long-term performance

Source: Bloomberg, S&P Dow Jones Indices, Refinitiv, and Eastspring Investments

Capture diversification benefits via multi-factor strategies

In the current market environment, where a narrow market rally driven by specific themes can lead to increased vulnerability, the need for diversification through multi-factor equity investing is paramount. Combining the wisdom of Aristotle, the insights of Markowitz, and a comprehensive understanding of the market landscape, investors can construct portfolios that capture the benefits of diversification and position themselves for long-term success.

By embracing a diversified approach, investors can navigate uncertainties, mitigate risk, and unlock the full potential of their investment strategies in the pursuit of sustainable returns.

Fig 3: 3-year rolling factor return pairwise correlations

Low volatility vs other factors

Peer relative value vs other factors

Quality vs other factors

Sentiment vs other factors

Short-term technical vs other factors

Momentum vs other factors

Source: Bloomberg, S&P Dow Jones Indices, Refinitiv, and Eastspring Investments

Interesting reads

Sources:

1 As at Jun 2023

2 Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 7(1), 77–91.

3 Merton, Robert C. "An Intertemporal Capital Asset Pricing Model." Econometrica 41, no. 5 (September 1973): 867–887. (Chapter 15 in Continuous-Time Finance.)

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.