Navin Hingorani

Portfolio Manager,

Global Emerging Market equities,

Eastspring Singapore

Apr 2025 | 5 min read

Executive Summary

- Global Emerging Markets (GEMs) appear to be at an inflection point, supported by resilient earnings and a likely peak in US exceptionalism. Attractive valuations and light investor positioning set the stage for the onset of an EM bull market.

- As sentiment towards China turns more positive, a potential resurgence of the Chinese equity markets makes a GEM ex China strategy even more relevant.

- A GEM ex China strategy mitigates China’s dominance of the EM Index, taps into the attractive opportunities that exist in the other EM markets and allows investors to express their views on China independently.

The sentiment towards China appears to be turning more positive, boosted by DeepSeek’s breakthrough and Chinese policymakers’ shift towards greater support for the economy. In our view, a potential resurgence of the Chinese equity markets enhances the benefits of a GEM ex China strategy.

A GEM ex China strategy gives investors access to attractive opportunities within EMs that are otherwise crowded out by China’s dominance of the EM index, while allowing them to manage their China exposures separately. Despite Chinese equities’ attractive valuations and potential upside, other factors may influence investment decisions. With China still very underrepresented in global equity indices and portfolios, its share and dominance of the MSCI EM Index will continue to grow. A GEM ex China strategy enables investors to independently express their views on this key market.

The declining correlation between MSCI China and MSCI EM ex China shows the rising diversification benefits of a GEM ex China strategy. See Fig. 1.

Fig. 1. MSCI China rolling 52-week correlations ve MSCI EM ex China

Source: FactSet, MSCI, Goldman Sachs Global Investment Research as of 7 March 2025. Charts are for illustrative purposes only. The index described is unmanaged and not available for direct investment.

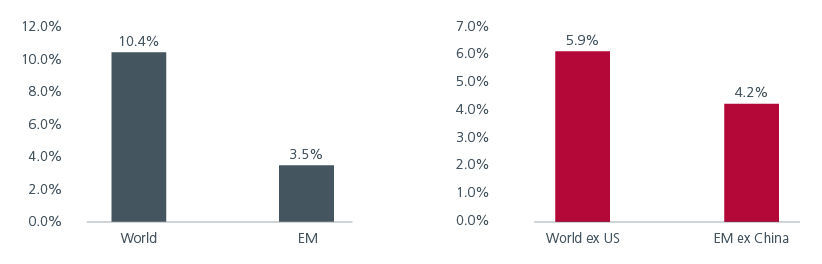

China’s large weighting (30.7%1 ) in the MSCI EM Index means that it has a large influence on EM returns. EM equities’ underperformance relative to Developed Market (DM) equities over the last 10 years was driven mostly by the Chinese market’s weakness and the US equities’ exceptional performance. The returns are more comparable if we exclude China and the US. See Fig. 2.

Fig. 2. Comparison of 10-yr annualised returns

Source: MSCI. As of end February 2025.

Spread your nets wider

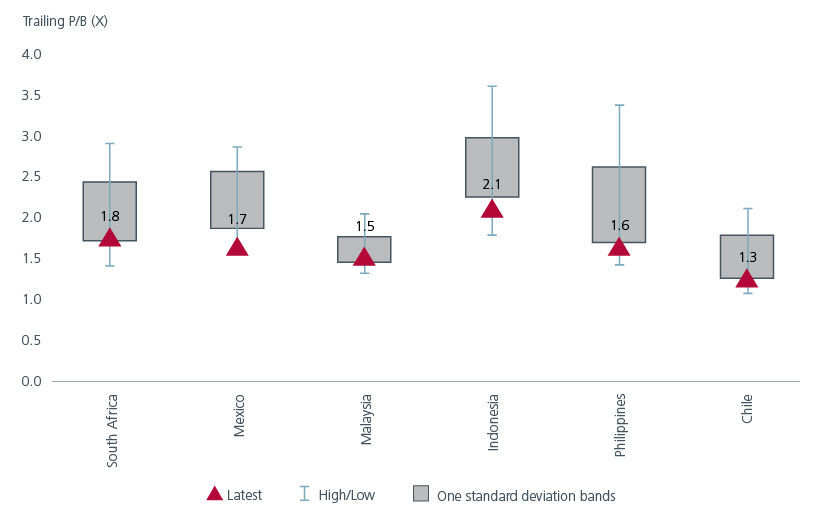

By excluding China from the GEM universe, investors can potentially access opportunities in other EM markets which may be overlooked in a traditional GEM strategy. Some of these markets are currently trading close to 1 standard deviation below their 10-year average valuations on a price to book basis. See Fig 3.

Fig. 3. Price to book valuations of selected EM markets

Source: Factset, MSCI, GS Global ECS Research, Eastspring Investments, Valuations as 31 December 2024. Index weights at 31 December 2024. Notes: PBx = Price-to-book ratio. Information herein is believed to be reliable at time of publication, and any opinion or estimate contained in this document may subject to change without notice.

Indonesia, for example, is forecasted to become the 4th largest economy by 2050 as it undergoes an economic transformation, partly fueled by its abundant reserves in transition metals. Indonesia’s economic growth should drive demand for consumer goods and financial services amongst its middle-class population. Meanwhile, the Brazilian market’s eye-catching valuations following last year’s poor performance are driving returns this year. While monetary tightening has impacted the economic outlook for 2025 and populist measures remain a risk, the declining government approval rates ahead of the 2026 elections have raised hopes for a new President and more rational fiscal policies. Additionally, the expectation that interest rates have peaked has boosted sentiment.

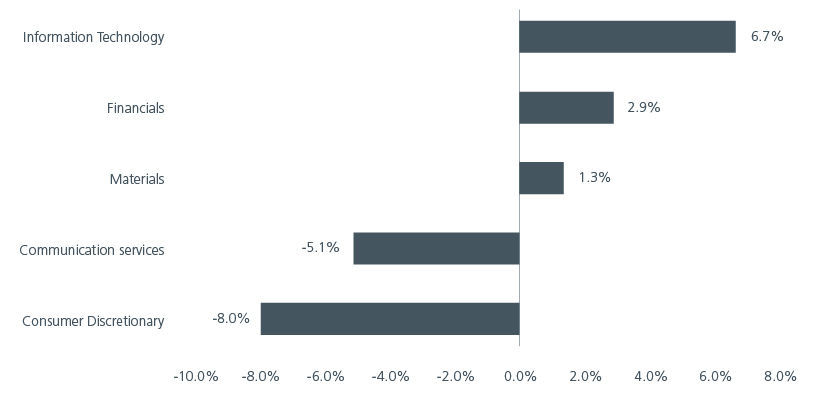

At the same time, the weightings of the technology and financial sectors are higher in a GEM ex China universe. See Fig. 4. While DeepSeek’s breakthrough has caused Chinese tech stocks to rally, our value approach leads us to find attractive opportunities in less “glamourous” names within the tech sector. Within financials, we are finding opportunities across various geographies. These opportunities are driven by prolonged higher interest rates and stronger loan growth, which is fueled by greater government and corporate capital expenditures, as well as a rise in consumer loans.

Fig. 4. Difference in sector weights – MSCI EM ex China vs MSCI EM

Source: MSCI. As of end February 2025.

More agility in a post-tariff world

Active investing has historically been more effective in the EMs versus DMs given the EMs’ market inefficiencies and lower information transparency. Going forward, active investing will probably be even more important as tariffs create primary and secondary impacts on EM countries and companies. While countries outside of China such as Mexico and Vietnam have benefitted significantly from supply chain diversification during Trump’s first term, there is now greater scrutiny by the Trump administration on countries that may be used by China to circumvent tariffs. With Mexico also in the line of tariff fire, EM investors would need strong research capabilities to navigate this complex backdrop. A GEM ex China universe may also include a greater number of small to mid- capitalisation stocks which tends to have less research coverage, hence requiring an active approach to generate alpha.

Rethinking EM allocations

Having underperformed DMs since 2010, EMs appear to be at an inflection point. This shift is supported by a potential peak in US exceptionalism and the USD, widening growth differentials versus the DMs and resilient earnings. Additionally, attractive valuations and light investor positioning set the stage for the onset of an EM bull market.

A GEM ex China strategy mitigates China’s dominance of the EM Index, taps into the attractive opportunities that exist in the other EMs and allows investors to express their views on China independently. With the rebound in Chinese equities year to date, it is even more relevant for investors to rethink their EM strategies.

Interesting reads

Sources:

1 MSCI. As of end February 2025.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.