Executive Summary

- Vietnam equities delivered annualised returns of 8.5% p.a. (in USD terms) over the last five years. Additionally, their low correlations with the developed markets help them to provide investors with enhanced portfolio diversification.

- The Vietnam equity market allows investors to participate in a dynamic economy with opportunities that tap into the country’s manufacturing competitiveness, digital transformation and growing middle class.

- Vietnam’s bid for emerging market status can potentially result in greater investor interest and inflows. However, addressing the challenges related to settlement procedures and foreign ownership caps remains crucial.

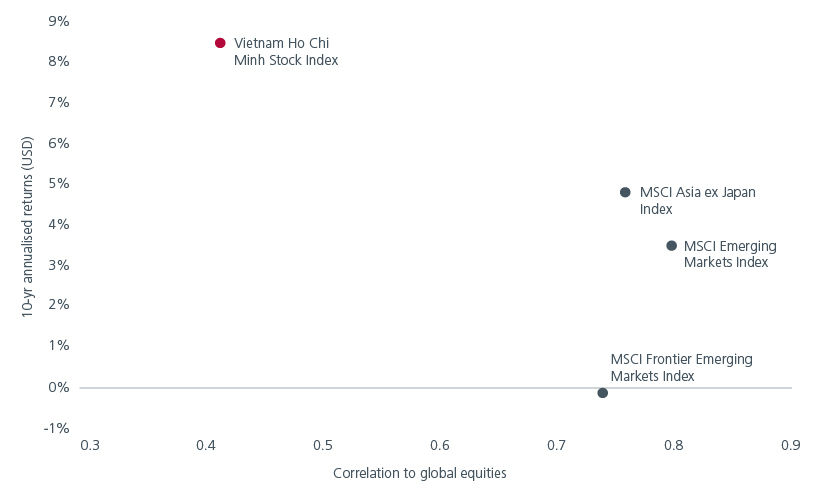

Over the last five years1, the Vietnam Ho Chi Minh Stock Index (VNINDEX) delivered annualised returns of 8.5% p.a. (in USD terms), outperforming both the MSCI Frontier Emerging Markets and MSCI Emerging Markets Indexes. More importantly, Vietnam equities exhibit lower correlations than MSCI Emerging Markets to developed markets, potentially providing investors with enhanced portfolio diversification, although with greater volatility. See Fig. 1.

Fig. 1. Correlations vs annualised returns

Source: Bloomberg. Annualised returns in USD terms as of 10 May 2024. 10-year correlations using weekly data in local currency terms, as of 13 May 2024.

Exciting opportunities

Vietnam’s robust economic growth is expected to help underpin the equity market going forward. The IMF forecasts Vietnam’s economic growth to expand 5.8% in 2024 and 6.5% in 2025, up from 5% in 20232.

Supply chain shifts

Global supply chain shifts have boosted Vietnam’s growth, with the country often referred to as the “China plus one” destination. Vietnam benefits from its cost-effective manufacturing capabilities and skilled labour force. Its proximity to China also facilitates streamlined logistics and efficient coordination between suppliers and manufacturers. At the same time, Vietnam’s status as a net energy exporter and its increasing efforts to diversify its energy sources to include renewable energy enhance its energy security and sustainability.

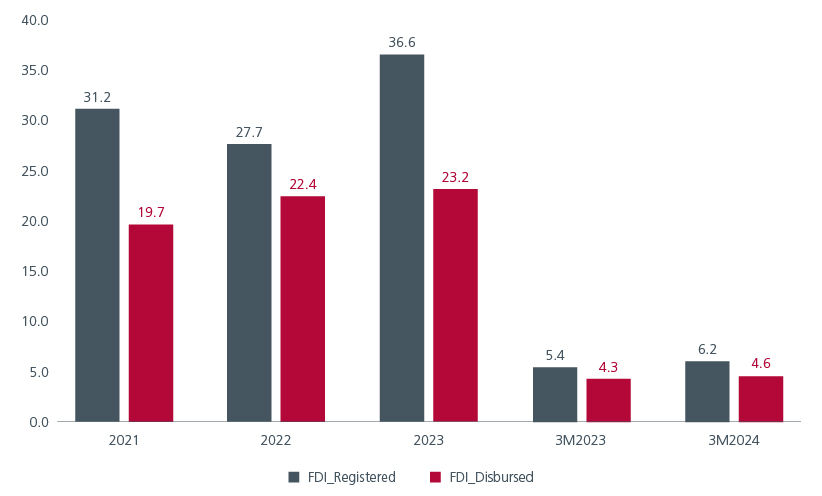

Vietnam attracted USD36.6 billion in foreign direct investment (FDI) in 2023, of which USD23 billion was disbursed, representing the highest level of FDI in Vietnam in the recent five years. The processing manufacturing sector received 64% of the total FDI capital. For 2024, total newly-registered FDI reached USD6.2 billion, representing a 13.4% year-on-year increase. Fig. 2. As the government continues to actively promote FDI through favourable policies including tax incentives, exemptions and streamlined administrative procedures, these investments should boost jobs, infrastructure development and overall economic growth.

Fig. 2. FDI into Vietnam (USD billion)

Source: General Statistics Office of Vietnam, as of 31 March 2024.

Growing FDI inflows are expected to drive industrial park (IP) demand, which should support rents. We like developers that can create a complete IP ecosystem by linking IPs with residential homes, utilities and social infrastructure as well as those that have large leasable areas to meet the needs of global manufacturers.

Digital transformation

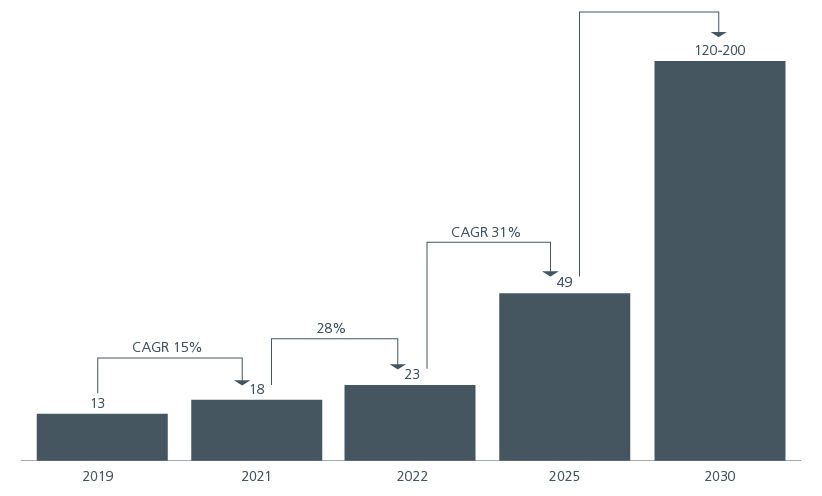

We also see opportunities in technology companies that can leverage on the government’s ambition to accelerate digital transformation within the country as laid out in the Digital Transformation Agenda. Domestic spending on digital infrastructure is expected to be significant amid rising digitalisation across industries, following years of underinvestment. The gross merchandise value of Vietnam’s digital economy in 2022 was USD23 billion, and is forecasted reach USD49 billion in 2025, largely driven by the e-commerce sector.

Fig. 3. Gross merchandise value of Vietnam’s digital economy (USD billion)

Source: Vietnam’s digital economy value and compositions. Bain Report 2022.

Rising middle income

The couThe country’s robust economic growth has also created a rapidly expandingntry’s robust economic growth has also created a rapidly expanding middle income population. Investing in Vietnam’s equity market potentially provides exposure to sectors such as retail, real estate, and consumer goods that stand to benefit from rising disposable incomes. Vietnam’s banks are increasingly focusing on the still-underdeveloped retail banking segment to diversify their income streams and improve profit margins. Digitalisation is also helping to reduce operational costs and supporting earnings growth. Compared to their ASEAN peers, Vietnamese banks generate higher return on equity (ROE).

Emerging market bid

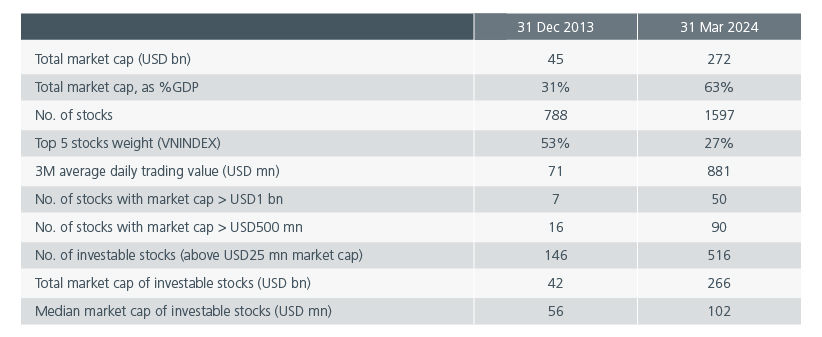

Vietnam is committed to strengthen its capital market to drive economic growth and stability. The equity market has grown rapidly over the last decade in breadth and depth (Fig. 4.) With the equity market’s current capitalisation averaging 60% of GDP, the government aims to raise market capitalisation further to 100% and 120% of GDP by 2025 and 2030, respectively. The government’s crackdown on corruption also demonstrates its commitment to maintain a more transparent and investor-friendly environment.

Fig. 4. Vietnam’s equity market has grown rapidly

Source: Bloomberg data as of 31 March 2024, computed by EIVN. Note: VNINDEX = Vietnam Ho Chi Minh Stock Index.

Vietnam has been working towards achieving an emerging market status by July 2025 which can potentially result in greater investor interest and inflows. However, addressing the challenges related to settlement procedures and foreign ownership caps remains crucial. On this front, Vietnam is piloting a trading system to resolve the need to have available funds before an order can be made, as well as to shorten the settlement cycle, although the system has yet to be officially launched.

Promising potential

The Vietnam equity market allows investors to participate in a dynamic economy with promising potential. The market’s return on equity had averaged 14.6% over the last five years, surpassing its ASEAN peers, and is forecasted to remain relatively steady at 14% in 20253. Whether it is tapping into Vietnam’s manufacturing advantages, leveraging on the country’s digital transformation, or capitalising on its growing middle class, Vietnam presents an exciting opportunity for long-term investors.

Interesting reads

Sources:

1 As of 10 May 2024. Bloomberg.

2 IMF. April 2024.

3 Bloomberg. As of 16 May 2024.

The information and views expressed herein do not constitute an offer or solicitation to deal in shares of any securities or financial instruments and it is not intended for distribution or use by anyone or entity located in any jurisdiction where such distribution would be unlawful or prohibited. The information does not constitute investment advice or an offer to provide investment advisory or investment management service or the solicitation of an offer to provide investment advisory or investment management services in any jurisdiction in which an offer or solicitation would be unlawful under the securities laws of that jurisdiction.

Past performance and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the strategies managed by Eastspring Investments. An investment is subject to investment risks, including the possible loss of the principal amount invested. Where an investment is denominated in another currency, exchange rates may have an adverse effect on the value price or income of that investment. Furthermore, exposure to a single country market, specific portfolio composition or management techniques may potentially increase volatility.

Any securities mentioned are included for illustration purposes only. It should not be considered a recommendation to purchase or sell such securities. There is no assurance that any security discussed herein will remain in the portfolio at the time you receive this document or that security sold has not been repurchased.

The information provided herein is believed to be reliable at time of publication and based on matters as they exist as of the date of preparation of this report and not as of any future date. Eastspring Investments undertakes no (and disclaims any) obligation to update, modify or amend this document or to otherwise notify you in the event that any matter stated in the materials, or any opinion, projection, forecast or estimate set forth in the document, changes or subsequently becomes inaccurate. Eastspring Investments personnel may develop views and opinions that are not stated in the materials or that are contrary to the views and opinions stated in the materials at any time and from time to time as the result of a negative factor that comes to its attention in respect to an investment or for any other reason or for no reason. Eastspring Investments shall not and shall have no duty to notify you of any such views and opinions. This document is solely for information and does not have any regard to the specific investment objectives, financial or tax situation and the particular needs of any specific person who may receive this document.

Eastspring Investments Inc. (Eastspring US) primary activity is to provide certain marketing, sales servicing, and client support in the US on behalf of Eastspring Investment (Singapore) Limited (“Eastspring Singapore”). Eastspring Singapore is an affiliated investment management entity that is domiciled and registered under, among other regulatory bodies, the Monetary Authority of Singapore (MAS). Eastspring Singapore and Eastspring US are both registered with the US Securities and Exchange Commission as a registered investment adviser. Registration as an adviser does not imply a level of skill or training. Eastspring US seeks to identify and introduce to Eastspring Singapore potential institutional client prospects. Such prospects, once introduced, would contract directly with Eastspring Singapore for any investment management or advisory services. Additional information about Eastspring Singapore and Eastspring US is also is available on the SEC’s website at www.adviserinfo.sec. gov.

Certain information contained herein constitutes "forward-looking statements", which can be identified by the use of forward-looking terminology such as "may", "will", "should", "expect", "anticipate", "project", "estimate", "intend", "continue" or "believe" or the negatives thereof, other variations thereof or comparable terminology. Such information is based on expectations, estimates and projections (and assumptions underlying such information) and cannot be relied upon as a guarantee of future performance. Due to various risks and uncertainties, actual events or results, or the actual performance of any fund may differ materially from those reflected or contemplated in such forward-looking statements.

Eastspring Investments companies (excluding JV companies) are ultimately wholly-owned / indirect subsidiaries / associate of Prudential plc of the United Kingdom. Eastspring Investments companies (including JV’s) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.